Quick quiz: He is the world’s third-richest person and the second-richest billionaire in the United States, after Bill Gates. Who is he? If you’ve not been living under a rock for the past couple of decades, you surely know who Warren Buffett is. You might not know that he was only 11 years old, when he bought his first stock—and he still managed to turn a profit. The rest is history, as they say. He’s made billions over time, picking his investments wisely and sticking to a few simple rules. And, while Warren Buffett may not be a penny stock trader, you shouldn’t be afraid to take some cues from the big boys. Here are 4 tips from Warren Buffett that we’ve adapted for the penny stock day trader: 1. Never lose money In Buffett’s words: “Rule #1 is to never lose money. Rule #2 is to never forget Rule #1.” We’re putting in our two cents here, though: When you digest the “never” in this tip, don’t get caught up in immediacy. It doesn’t necessarily mean “don’t lose money on a single trade.” It means, don’t lose money at the end of the day. Every investor has taken a loss. The trick here is to stay sober and keep emotion from guiding your investment decisions. Be smart, stay informed and don’t ‘gamble.’ Avoid temptation, because as soon as you feel something that can be described as ‘tempting,’ it’s emotion talking. Everyone will lose in the beginning, because that’s part of the learning curve. You have to be ready to accept these losses. These losses are investments in your education. What’s important here is that when you emerge, it’s with more money than you started with. Never lose—overall. We appreciate the ‘never lose’ sentiment, coming from a man who made his first stock win as an 11-year-old boy—but not everyone is a Warren Buffet and learning curves are varied. 2. Limit what you borrow Avoid funding your trading account with loans. What’s the point of risking someone else’s money and possibly piling up debts to pay for whimsical trades, when you don’t have a hundred dollars in the bank? This is where we kindly remind you to put a borrowing limit on yourself, before you start trading and even before you create and fund your own trading account. That’s how you’ll know your maximum possible losses. And, you’ll remember to stick to rule #1, which you should never, ever forget, according to our favorite self-made billionaire and the second-richest person in the U.S. “Limit the borrowing” also means: don’t tap into your rainy-day funds and don’t use credit cards to finance a venture that is way riskier to take when the money is not yours to spend. Instead, try taking on (and winning over) the trades, one step at a time, with funds over which you have control. These are real wins and lasting wins. If you need some help saving up for your trading account, check out our blog post with some tips on funding your account. 3. Live simply That’s Buffett’s way. Even though his net worth, as of the end of September 2016 is a mind-boggling US$65.1 billion, Buffett lives in a modest home in his native city of Omaha, Nebraska. He has been getting a base annual salary of US$100,000 from Berkshire Hathaway for the past 25 years. Our take? First, have your expenses covered. Then, enjoy life the way you want to. If your perspective is that success means working just a few hours a day, rather than slaving away at a 9-to-5 job, that’s fine. If it’s about buying a luxury sports car, that’s also fine. The point is, be happy with your choices, do what you love and love what you do. Don’t spend to spend and never spend to show off. Here’s how Buffett has described success: “Success is really doing what you love and doing it well. It’s as simple as that. Really getting to do what you love to do every day – that’s really the ultimate luxury… your standard of living is not equal to your cost of living.” Yes, it’s as simple as that, according to this billionaire trader. When you love your life, you’ll find it much easier to follow our final tip: 4. Stay optimistic Buffett is optimistic about markets and investments and sees opportunities in bull and bear markets alike. Take this piece of advice and know that prolonged bear market runs can present exciting and lucrative opportunities for trading penny stocks. Don’t follow the crowd. Stick to your investment strategy. Market sentiment and trends are constantly moving up and down, often in a matter of seconds. So, don’t be afraid of volatility and inconsistency: that’s the way it works, after all. If you have done your homework, assessed the risks and understood your loss and borrowing limits, then any kind of market will be a great investment opportunity. Just keep calm, believe in yourself and don’t give up. As the late William Feather, the author of The Business of Life, famously stated: “One of the funny things about the stock market is that every time one person buys, another sells and both think they are astute.”  Many consider Warren Buffett, the world’s fourth wealthiest individual, is the greatest investor in the previous century.

Mr. Buffet is well-known for his patent folksy insight on money matters and continues to provide many investors with valuable investment advice. Here is a rundown of what many consider Warren Buffet’s best investment tips (not including the latest stock picks): 1. “It is better to buy a wonderful company at a fair price than a fair company at a wonderful price.” (From a letter to shareholders in 1989) This advice from Buffet is a favorite quote of many investors. It contains a fundamental principle he has used effectively for years as his strategy for investing. Essentially, he chooses firms which he can completely understand and whose innate worth is clearly apparent, no matter what its present financial condition might be. Today, Buffet is # 4 only because he gives out large sums of his money to charity; otherwise, he would be the top choice -- like he was in 2008 in Forbes' choice of the richest person worldwide. Buffett started his enterprising journey in Omaha, Nebraska as a boy selling magazines and chewing gum to families. At 14, he filed his first tax return (claiming deductions for his watch and the bike he used on his paper route). He and a friend purchased and operated a pinball machine when he was in high school. The two also set up a town barber shop and later on expanded the business around town to incorporate pinball machines. Currently, Mr. Buffett has a personal net worth of about $55 billion and his investment company, Berkshire Hathaway, completely owns several reputable U.S. firms, such as Dairy Queen, Helzberg Diamonds, GEICO and 50% of Heinz. 2. “Rule No. 1: Do not lose money; rule No. 2: Remember Rule No. 1” (From "The Tao of Warren Buffett", 2006) 3. “Our approach is very much profiting from lack of change rather than from change. With Wrigley chewing gum, it's the lack of change that appeals to me. I don't think it is going to be hurt by the Internet. That's the kind of business I like.” (From Businessweek, 1999) Berkshire Hathaway's portfolio proves that Buffet practices what he preaches: The company invests principally in firms that have operated for many years and can be described in a few words: GEICO sells insurance, Dairy Queen sells ice cream, etc. The story of how Buffett's relationship with GEICO began goes back as early as 1952, at the time he sought to meet one of his investment idols, Benjamin Graham, who sat on GEICO's board. He ended up accidentally meeting the firm’s vice-president then, Lorimer Davidson, who has become Buffet’s close friend since then. 4. “The stock market is a no-called-strike game. You don't have to swing at everything – you can wait for your pitch. The problem when you're a money manager is that your fans keep yelling, ‘Swing, you bum!’“ (From "The Tao of Warren Buffett", 2006) 5. “I try to buy stock in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.” (From a panel discussion after the documentary premier of "I.O.U.S.A", 2008) 6. “Price is what you pay; value is what you get. Whether we're talking about socks or stocks, I like buying quality merchandise when it is marked down.” (From a letter to shareholders in 2008) Shareholders at Berkshire Hathaway eagerly await Warren Buffett's yearly letters and admire them for their great storytelling using simple and clear words. 7. “If you understood a business perfectly and the future of the business, you would need very little in the way of a margin of safety.” (From a Berkshire Hathaway annual meeting in 1997) 8. “Never count on making a good sale. Have the purchase price be so attractive that even a mediocre sale gives good results.” (From "Buffett: The Making of an American Capitalist", 1995) This signifies that a business that is quite unstable will also require a greater margin of safety in case you decide to invest in that business. For instance, if you drive a truck over a bridge that can only carry 5 tons and your truck weighs 4.8 tons and the bridge is less than a meter above a stream, you might feel much safer than if it were over a 20-meter ravine. 9. “We've long felt that the only value of stock forecasters is to make fortune tellers look good. Even now, Charlie [Munger] and I continue to believe that short-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children.” (From a letter to shareholders in 1992) Charlie Munger, also a native of Omaha, Nebraska, serves as vice-chairman of Berkshire Hathaway and has been Mr. Buffet’s business partner for many years. He also serves as Costco’s director. In spite of their close personal and business relationships, they differ in political preferences, Munger being a recognized Republican while Buffett has recently supported Democrats. 10. “We don't get paid for activity, just for being right. As to how long we'll wait, we'll wait indefinitely.” (From a Berkshire Hathaway annual meeting in 1998).  In the middle of positive signs for economic progress and with decreased focus on the bondholders’ interests, what should an investor do? We suggest these six timely tips.

Remain Actively Involved Managers who stayed active last year experienced a highly productive time, in part due to their tendency to steer away from hyper-cyclical one-theme sectors, such as resources which had a great recovery last year, and in part due to paradigmatic policy changes during the same period. The dominant macro-economic forces caused stock pickers to react slowly; however, with fresh themes appearing on the horizon, active managers looked at enough valuation anomalies to exploit. Focus on Value Valuations in the equity market stay higher than their averages over the past, in part due to low earnings in some sectors and in part due to the valuation driven drastically by low interest rates. Few windfalls can be derived from index levels; thus, be very picky when choosing within and between markets. Never Assume or Overreact Although political risks abounded (remember the UK exit from the EU, the rush of European elections and the entry of Trump on the scene – referred to as 'known unknowns'?) a lot of complaints, I know, 2016 taught us that anticipated reactions could totally misjudge the import of new political developments. For instance, Brexit has certainly made predicting the UK economy more difficult; but the dip in the value of the sterling has enhanced the prospects of earnings in the corporate sector. Predominantly, developments in 2017 could raise short-term volatility with the ultimate outcome being brought about by economic events. As the saying aptly says, the markets are short-term voting machines but long-term weighing machines. While greater growth and increased inflation can both appear highly possible, debt levels, technology and surplus supply work together as a secular force to prevent inflation; on the other hand, any fiscal package is slow to resolve and enforce, thus, the impetus for growth may also take time to work. Trapped in Bonds Many of us know that Ian Fleming never wrote some of the Bond movie scripts; and so, investors have an alibi for wondering whether a bond which charges interest (rather than paying) is an asset or a liability (or, maybe seen as a temporary security). Aim for Freedom of Thought The present world is not more a post-factual world than a post-truthful news machine. Eventually, the truth returns with a vengeance when people who trust untruths fall along the way. Make up your own mind; there is no other way – just make sure you get advice when needed. This is because people rush into buying during high markets and into selling going into a dip. The rule to follow in this case is: Be greedy only when others are fearful and be fearful when others are greedy. Be Practical Be an optimist. With the advent of active management and the progress of human endeavors through the centuries, it always pays to support and to look forward to progress. Nature teaches us innumerous lessons on adaptability, a skill as widely valuable in finances as in the jungles of South America; and 2017 will surely have its share of events that will challenge our skills in reacting to difficult situations.. Check valuations closely. Equity valuations may seem high but reasonable, considering low revenues in other places, while public bond yields may seem to provide low investment value, but unthinkable under normalized conditions. Avoid hoping for substantial returns from equities from this stage; although corporate earnings seem to be improving – it all depends really on how the growth interacts with valuation challenges as interest rates increase. Considering that long-term UK government bonds produce less than the Bank of England's inflation goal, it might be difficult to predict how returns (before tax) will fare any better than inflation and quite easy to foresee how they will do worse.  With the New Year 2017 here now, people find themselves again looking for ways to build financial resolutions to help them ultimately succeed. In a recent study involving over 5,000 American adults, the three resolutions at the top of the list were, in order: to save more, pay off debt and improve income.

Whereas enhancing savings and reducing one’s expenses make for a good beginning as well as bring lasting benefits, one need not stop there. For those who may feel their present financial status needs a makeover or simply want to change the way they deal with money, here’s 10 suggestions to formulate effective financial resolutions. 1. Set flexible objectives. Within the past 12 months, what major changes in your finances have you observed? Do you expect them to change within the following 12 months? Did you ever set any financial objectives before? If you are not certain, do not fret – this could be the perfect time to begin. Distinguish your objectives into two classes, long-term and short-term. After that, you can chart your own map to achieving both types of goals. 2. Establish a more efficient spending program. This is an indispensable and essential tip, one that must form as the foundation for each financial decision you will make. Write down all your expenses and subtract it from your salary to find out how you fare in your finances. Some of your expenses may have to be reduced to leave some money for vital needs while living within your means and fulfilling your future financial aspirations. 3. Set up an emergency fund. The same with increasing your savings and reducing expenses, setting up an emergency fund also strengthens your overall financial health. There will always be unexpected expenses along the way; however, being prepared reduces any adverse effects. Financial experts recommend putting aside an emergency fund to cover three to six months of your living expenses in case you lose a job or need medical attention. 4. Set aside money for a down payment. With the economic crisis limiting access to credit, buying a home, which is every non-homeowner’s dream, has become even more difficult. If you are one of those who have this long-term goal, save some of your money now. Be prepared to put down 10 to 20 % of the price of your dream house, depending on the real estate prices in your locality. Paying 20 % down payment allows you to waive a private-mortgage insurance; so make this your target level. While it is harder to achieve, it will help you follow the save-more/spend-less mantra in the long run. 5. Pay your big debts first. Although most people want to pay off all their debts, they fail to realize that not all debts have the same urgency. For instance, credit cards that charge high interests must be paid off ahead of others. Again, saving more money by spending less on interests is the rule. 6. Plan for your retirement. For many young people, planning for retirement may seem too early in the day; however, this misplaced attitude is actually counterproductive. In case you still do not have one, apply for an individual retirement account (IRA) – ask your CPA if a conventional IRA or a Roth IRA best suits your situation. Continue contributing to your 401(k) if your employer matches your regular payments. That is free money you can avail of for your benefit; so receive it by the good graces of your employer. Pay as much as you can on those contributions. 7. Regularly check your income tax situation and estate plans. Do you get a sizeable tax refund? Have you had changes in your tax payments? Do you receive only one income even though you are a two-income couple because you lost your job or went through pregnancy? Did you experience becoming self-employed after having been an employee previously or vice versa? Did you or your spouse retire and begin getting pension income or reach the wonderful age of 70½ and must now get mandatory IRA benefits? If so, you may have to adjust your withholding to avoid any adverse events. Moreover, you need not be so wealthy or own a yacht to need an estate plan. As long as you have assets, you need an estate plan. All the above questions will be answered sufficiently by your CPA; so, pay him or her a visit. 8. Be informed. Always be conscious about your financial well-being. Maintain a clean credit record, check your credit statements regularly and be aware of any changes. At the start of each year, resolve to read your credit reports. Monitor closely your bank account statements and credit card statements in order to avoid any imminent problems. 9. Seek professional help if needed. Ask your CPA once in a while in order to find out if you are well on your way to attaining your goals. When you need expert advice, get it; otherwise, do your share in keeping your finances on keel. 10. Wizen up. Although it is good to seek professional advice when needed, make sure you also know enough to take care of important decisions yourself. Get to know your financial situation and various investment opportunities. Attend seminars and classes; read books or magazines; and learn from others’ experiences and knowhow. Having sufficient knowledge allows you to have proper control of your financial welfare.  How’s your investing style?

The growing mutual funds industry owes its numerical growth partly to the assorted investing styles applied by capital managers. Research shows that investing styles greatly influence fund returns, fanning the debate in the financial community about their effectiveness. Here are the major styles utilized by contemporary fund managers. Passive vs. Active Passive investors believe that simple investments in a market index fund can create productive long-term benefits. Active investors, in contrast, trust their capability to overtake the entire market by picking promising stocks. The bulk of mutual funds performed below market indexes within the five-year period which ended on December 31, 2015.* Passive investors explain the result on market efficiency, the theory that considers all information reported regarding a firm is represented in that firm's present stock price; and that it is very difficult to predict and benefit on forthcoming stock price levels. Instead of trying to divine the market performance, what passive investors do is to buy the whole market through index funds. Active investors, in contrast, believe that managed funds will not always perform below the index level of the overall market. So many funds have attained substantially higher revenues. These active players see the market as not always efficiently running and that with research they can discover information not yet obvious in a security's price and thereby gain from it. For instance, some active investors consider small-cap market as being less efficient than large-cap market because smaller firms, in practice, are not monitored as regularly as bigger blue-chip companies. They explain this by the assumption that a less efficient market could prospectively favor active stock selection. *Source: Standard & Poor's, S&P Indices Versus Active Funds (SPIVA®) Scorecard, Year-End 2015. In the five-year period going to 12/31/2015, 84% of large-cap funds did not outperform the S&P 500 Index, 77% of midcap funds performed below the S&P MidCap 400 Index, and 90% of small-cap funds also underperformed the S&P SmallCap 600 Index. Value vs. Growth There are two kinds of active investors: growth and value hunters. Defenders of growth look for firms that can (on average) improve returns by 15% to 25%; although there is no certainty that this goal will be attained. These firms’ stocks usually have high price-to-earnings ratios (P/E) as investors shell out a premium for better revenues. And they often pay low dividends, if at all. This can result into more volatile growth stocks with greater risks involved. Value investors, on the other hand, hunt for low-priced investments -- bargain stocks which are usually out of favor, for instance, cyclical stocks dwindling at the tail end of their business life. A value investor is generally pulled into buying asset-based stocks with low prices vis-a-vis fundamental book, liquidation or replacement values. Value stocks, likewise, often have characteristically lower P/E ratios and higher prospective dividend benefits. These promising higher returns often protect value stocks in down markets, whereas some cyclical stocks will lead the market after a recession. Some investors prefer a more free style by choosing not to be locked into any single investment style. Revenues from growth stocks and value stocks often tend to be closely connected. That is, a decrease or increase in either can produce negligible effect on the other. By choosing to diversify between value and growth styles, investors can manage risk more effectively and still hope to gain potentially high, long-term benefits. Small Cap vs. Large Cap In other cases, some investors look at the size of a firm before investing. Research shows that stock returns way back in 1925 suggest that going "smaller is better." In general, small-cap stocks have overtaken large-cap stocks over the long-term durations. However, as these returns often go through cycles, there were long durations when large-cap stocks did better than smaller stocks. Small-cap stocks also go through more price fluctuations, leading to greater risks. Choosing the middle road, some investors choose to invest in mid-cap stocks with have market capitalizations from $500 million to $8 billion – finding a trade-off between return and volatility. By doing this, they give up the promising returns of small-cap stocks. Sources: Standard & Poor's; Center for Research in Securities Pricing (CRSP). Large-cap stocks are represented by the S&P 500 Index, an unmanaged index often considered representative of the large-cap, U.S. stock market. Small-cap stocks, on the other hand, are represented by a composite of the CRSP 6th-10th decile portfolios and the S&P SmallCap 600 Index, unmanaged indexes that are often considered representative of the small-cap, U.S. stock market. Top-Down vs. Bottom-Up A top-down investor observes initially economic influences and then chooses industries correspondingly. For instance, at low-inflation periods, consumer spending rises, a good time for purchasing retail stocks or automobile stocks. A top-down investor would therefore look for the highest values in such companies. In contrast, a bottom-up investor is chooses to consider the individual firm’s fundamentals. They believe that even if its industry is down, a hot company can still overtake the market. Both styles highlight fundamentals but put contrasting focus on the economic climate. Technical vs. Fundamental Analysis Then there is the difference between some equity investors in terms of the fundamentals of individual stocks and their technical characteristics. Fundamentalists, who outnumber technical analts, focus on yearly reports and visiting firms in trying to discover investment potentials and higher potential returns in the long haul. On the other hand, technical analysts closely monitor charts of stock prices and economic information to try to discover patterns which can predict future trends. They are more into observing short-term market performances instead of picking individual stocks. While technical analysts have failed to gain more adherent due to their questionable forecasting abilities, enhanced access to information and the rising capability of computers have driven greater interest among investors. Asset Allocation: A different form of investing "style" Asset allocation has become an acceptable form of investment style. Investors who are considered market-timing purists move in or out of particular types (bonds, stocks and money markets1), according to the projections of their technical models. A safer method, dynamic asset allocation, applies risk/return trade-offs to decide which class of assets to choose. Nevertheless, asset allocation does not ascertain success or safeguard against loss. If bonds are deemed "cheaper" than stocks, then allocation will work in favor of bonds. Those who allocate their assets regularly adjust their portfolios according to the market and economic environment. 1An investment in a money market fund is not guaranteed or insured by the Federal Deposit Insurance Corporation or any other government agency. Although the fund seeks to preserve the value of your investment at $1.00 per share, one can lose money by investing in the fund. Choose diversification when in doubt Many experts recommend diversification in order to manage fluctuations in the market as another investment style. Mutual fund investors have to do research and ask valid questions, read the fund prospectus carefully, and seek advice from fund-rating services to ascertain that they are buying a style that is right for them. You now have to decide which one -- or which ones -- of these styles is suited to your personal situation. Seek the assistance of an investment advisor help you go through the process of unraveling the issues in order to come up with your own unique style.  Although it is common practice for couples to share practically everything, keeping their finances strictly separate provides more advantages from an investing perspective.

You may not need to hold separate bank accounts as well as keep individual budgets. However, you can design your investments to maximize your income and benefit from tax regulations. Several reasons explain why many people think such couples get by on one income alone. A partner could be on leave from work to start a family or going to graduate school. Other reasons that keep you from your job could be personal or medical problems. No matter what the reasons are, in case you expect to stay that way for a couple of years or more, you have the option to protect yourself with some kind of investment plan to meet your needs. How to invest on a single income: Purchase in strategic names For those who earn above-average income, avail of the commonly used and efficient way to invest in property of negatively gearing your investments in order to get a tax refund and keep your investment cash-flow positive. How do you do this? Acquire the property under the name of the higher-income earning partner to offset the whole value of the present tax deductions against his or her income tax. Likewise, buying a property that is cash-flow positive before tax – although rare nowadays – under the name of the non-income earning partner will be a preferable choice since she or he will not pay tax on any earnings of or below $18,000. Invest in a family trust if you can If you set up a family trust and buy assets through it instead of in your own individual names, you could effectively save a big chunk of money in household tax fees. This is due to the fact that distributions can apply to lower-income family members or a no-income partner and children above 18 years old – since the trust is tax-free; however, the beneficiary will pay tax. Be aware that using a family trust will not allow you to spread any loss; hence, this kind of investment strategy will not fit negatively-geared assets. Make sure to consult with an accountant or financial counselor prior to choosing the purchase strategy to use to understand what the best options are in your particular situation. Get life insurance and income safeguards Having an income safeguard and life insurance is vital for all investors since such instruments will serve as hedge against illness or demise. For those couples with only one income source and one of them is the sole family income-earner, then protecting your income and insuring yourself should be done. Having life insurance provides a lump sum to the remaining partner and secures the financial well-being of the orphaned family members. On the other hand, having an income safeguard will cover 75% of your present regular salary in case you become disabled before reaching 65, leaving you free and not burdened financially while you recover and seek treatment. Inexpensive protection for only two years is clearly insufficient. Take note that all advices or tips given here should not be considered as financial or taxation advice but given only as recommendations for the reader. You need to do further study and investigation on how to evaluate your own particular financial status. Seek the expert assistance of your accountant to see how any financial decisions will impact your overall situation. With reference to the previous week’s article on our tax laws pertaining to offshore investment fund property (OIFP) rules and the recent court decision on Gerbro Holdings Co. v. The Queen, avoiding the OIFP rules, as Gerbro did, can actually benefit investing outside of Canada. In the case of Gerbro, the investor had valid reasons for offshore investment which aimed neither to reduce nor to defer tax – winning the case in the process. How will this affect you as an investor?

The rules Under applicable rules, you will be taxed by adding to your income a certain amount per year in the amount of your offshore investment times the present 3 per cent interest rate. (The 3% rate is two percentage points more than the stipulated present interest of 1%). You are entitled to deduct from this assumed income figure any other income (except for capital gains) included on your annual tax statement from the offshore investment. Moreover, any deemed income will be augmented to the adjusted cost base of your offshore investment. Ultimately, these requirements accomplish two things: First, you are paying tax before receiving the income, and second, they allow you to consider as regular income that which should be taxable as capital gain. As an illustration: If you have invested $300,000 in offshore funds. Using OIFP rules, you pay tax, since a major goal of the investment is to reduce or defer tax, on the deemed income of $9,000 (3 per cent multiplied by $300,000). A payable tax of $4,500 based on a 50% marginal rate. Under cases of tax deferral or avoidance as a primary objective for the investment – which means OIFP rules do not apply – taxes may still be applicable using the same rules, leaving you the choice to file a case in court. However, majority of investors will accede and pay the tax and will then decide to alter their investments in this case considering that accounting and legal fees to sue the Canada Revenue Agency will certainly be higher that the tax due under the rules in question. CRA is well aware of this. It will not hesitate to harass taxpayers for as low as an imputed income below $10,000, showing how unfair and abusive CRA can become. Why should CRA take steps to unduly increase tax due and lead Canadians to choose investment options not designed to attain their long-term objectives. Remember, CRA can pinpoint these investors using Form T1135, filed annually by investors outside of Canada in amounts above $100,000. CRA believes these investors are out to avoid tax. Heads up, CRA: Why would taxpayers report such investments on their Form T1135 if they mean to avoid tax? Look for evaders somewhere else! Tips for Investing Accomplish an Investment Policy Statement (IPS) Ask an investment manager to accomplish an IPS for you, which is a vital document you need. An IPS must include specific investment information, such as your investment goals and risk capacity. Make it very clear that you have valid reasons for your offshore investment and that they do not include reduction or deferral of tax. Discuss Your Documents Sit down with your investment counselor to explain your investments goals and make it very plain that tax reduction is not among your primary reasons for your investment and include such discussions in your prepared meeting minutes. Those minutes should be kept on file as proof of your reasons for choosing the offshore investment. Monitor your investment cost For investments in offshore property below the total value of $100,000, you need not reflect such assets on CRA’s Form T1135, keeping you out of its screen. Keep dreaming of that time when CRA hikes up the golden standard below which the agency will not make any fuss about your intentions for investing in offshore funds.  A good investor needs to develop the discipline to buy low and sell high. Such discipline can only come from sufficient experience, particularly through the process of learning from one’s mistakes and gaining the knack for making with better decisions.

The mantra for successful investing is: Buy low, sell high. Obviously, this applies in almost all forms of enterprise. Yet, in investing, this rule is rarely observed by most people, making it hard for an individual to follow since the rule-of-the-mob prevails. What to do? The following steps will help us recognize whether an investment has great potential or not: 1. Step one is to buy low. Determine what the base line is for an investment and bide your time until the buying price goes down below the reasonable level. This is the same time when people panic and sell as the stock market dips. That is your signal to hunt for buying opportunities. The best way is to buy an asset once the price drops substantially, waiting for a time when it climbs and brings a significant gain. 2. Step two is to sell high. Ideally, the right time to sell an asset is when the price rises substantially. During such time of stock market growth, people are buying everywhere. That is the best time to sell in order to maximize your gains. With the money in your hand, you can then repeat the process by looking for a low-performing asset or any secure investment. 3. Recover from your mistakes. No matter what you do, mistakes are bound to happen. Buying low and selling high, after all, is not a fool-proof method. Losing money happens wherever you go and whatever you do; so, try to roll with the punches and learn to pick up the pieces. After recovering from a hard fall or loss, slowly pace yourself back to your former condition by making some market gains through an index fund. Or perhaps, take time to evaluate carefully an investment prior to risking a sizeable amount of your money. Fear tends to terrify and immobilize a person and keep one from reaching your highest potential. Instead, let courage propel you to newer heights of success. 4. Do self-evaluation. Assess all the past investments you have made and determine how you can obtain better results in the future. Writing down your thoughts and insights will assist you to clarify in your mind how to avoid future traps along the way. Moreover, a visible road map will help keep you from making decisions based purely on emotional fancies. A professional investment expert or a financial planner and a tax planner can also help you evaluate your investment ideas, increasing the reliability and accountability of your financial plans. 5. Establish a plan and stick to it. Losing big-time in investing can lead to much regret. Likewise, you may also regret not having invested in an asset that has soared beyond your reach. Planning well and doing meticulous analysis will help significantly in preventing failure. A written plan will also serve as a firm guide to prevent you from being easily swayed by people around you. You may also utilize the planning stage to fine-tune your main aspirations in life and determine how your finances will become instrumental in realizing them. People invest in order to achieve and sustain a lifestyle of their choice. Succeeding in your investment choices will build sufficient wealth for an early retirement or to escape an undesirable job. To assure your success in this endeavor, you must apply reason and follow a financial plan to build your personal wealth. On the other hand, being merely led by the latest investment trend does not comprise a solid plan of action. It is time to take control of your finances and your life.  Warren Buffett’s success in the stock market using a common-sense approach is no secret. Nor is his enormous wealth he has accumulated through Berkshire Hathaway, the holding company of his middle-American companies, which he acquired in 1965 as a former textile and garment manufacturing company.

What are secret are his specific strategies to successful investing. But we can learn from Mr. Buffett by imitating 10 ways he openly does it, namely: 1. Simple logic does it. Anything that is used daily and entrenched in the economy is represented in the portfolio of Berkshire Hathaway. For instance, energy, retail, finance, utilities, insurance, manufacturing and railroads are industries which are essential to the ordinary consumer. More so with “grocery cart” brands which represent timeless needs and which Buffett translates into long-term, consistent values. Moreover, Berkshire Hathaway interests also include Duracell battery, GEICO insurance and Wells Fargo finance. For Buffett and his workers, if you use it often enough, why not own a part of it? 2. Character has real value. LouAnn Lofton, who wrote “Warren Buffett Invests like a Girl and Why You Should, Too”, says that Mr. Buffett invests only in companies whose management he likes and trusts. According to her, how the management treats its stakeholders and the public, in general, and how the public perceives the management as well, provide solid indicators of the excellent performance of the company. That company deserves an investor’s trust and investment. 3. Determine Core Value. Roy Ward, chief analyst of Cabot Heritage Corporation in Salem, Massachusetts, criticizes firms which often complicate their financial reports with one-time “extraordinary expenses”. Although you may not have the many analysts that Buffett has, Ward says that you can still detect the indicators of core value. She defines “core asset” as one which you would buy, be it a firm engaged in real estate or intellectual property. She advises the investor to monitor the “book value per share” of a company which represents the core value of the company compared to the current stock price. 4. Headlines are undependable. BAM Alliance director and author, Larry Swedroe, who wrote “Think, Act and Invest like Warren Buffett”, says that there is no lasting value in trusting what the financial headlines proclaim. He says it is better to walk a few steps ahead of the headlines. According to Swedroe, while it is difficult to predict what the market, the Federal Reserve and the government will do, any investor can tell that the government will act to stabilize the economy. Based on that general knowledge, the opportunities will come. 5. Learn fundamental performance metrics. Ward says that once you grasp the book value of an asset, determine how much the firm makes on its assets. If you are Buffett, you would want at least 20% return on the assets which eliminates so many companies from the picture, Ward adds. Likewise, monitor the trend lines, looking for firms that made 10% in the past and now makes 20%, as that indicates good performance. Why that is so is something you would want to know -- what Buffett is also interested in. 6. Be Patient. If you know of companies that fit Buffett’s targeted investments choices, keep your eyes on them, Ward advises, in order to see how they fare in the market and how their stock price is valued. If a firm consistently makes money but its stock price does not keep up with its book value, then you have a potential asset to buy and hold. 7. Opt for the long-haul. Lofton says that buying and holding eventually builds wealth although majority seek to gain over a short-term range. Buffett, according to Lofton, has his eyes on the everlasting results, which she describes as seemingly “lethargic or slothful”. She advises that for the rest of us, holding on for five years is enough. Statistics prove that it takes that long to complete a market cycle, she adds. 8. Monitor Buffett’s reports. In general, corporate annual reports are known for their slanted and toe-the-liner statements. Berkshire Hathaway reports, on the other hand, are simple and unpretentious. This is because Buffett tells his story in plain English, narrating what he and his team did, how they did it and why, keeping the reader interested. 9. Invest in index funds. In case the previous steps seem to require too much work, Buffett recommends buying index funds, according to Swedroe. This is because investing in index funds allows an investor to overtake majority of stocks and industries.  Get started with Frank Owens Limited Advisor Services.

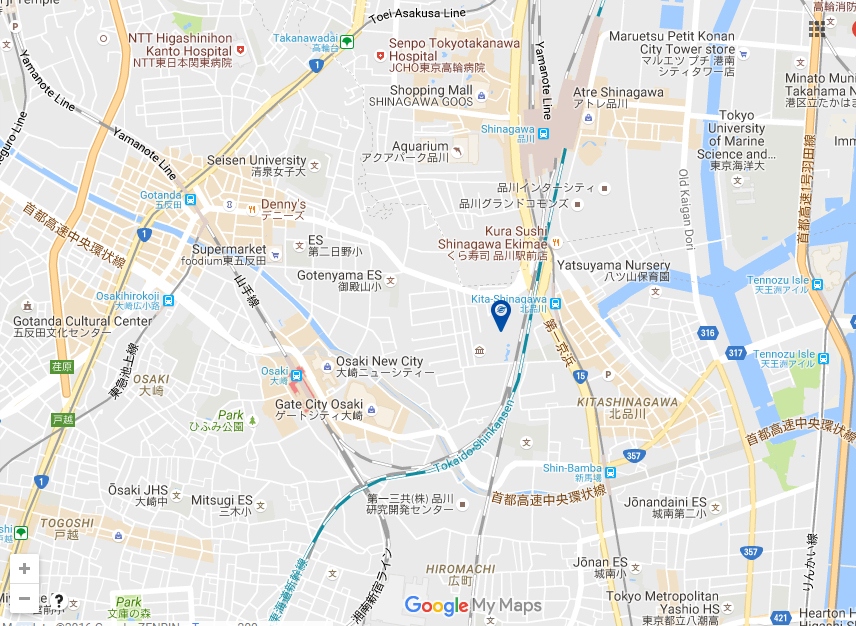

Speak with a specialist who's experienced with helping high-net-worth clients. Address: 17F, Gotenyama Trust Tower, 4-7-35, Kitashinagawa, Shinagawa-ku, Tokyo, 140-0001, Japan Telephone: +81343301948 Telefax: +81367000965 Email Address: [email protected] Website: http://frankowenslimited.com/ |

About UsFrank Owens Limited provides a broad range of professional financial advice to entrepreneurs and business managers with respect to the most appropriate steps in acquisition, disposition and funds sourcing, based on the present market conditions. Archives

12 月 2016

Categories |

RSS フィード

RSS フィード